Mexico’s Opportunity Is Real. So Is Its Regulatory Architecture.

Mexico has rapidly emerged as one of the most strategically important destinations for global manufacturing and supply chain realignment. Nearshoring momentum, access to the U.S. market through USMCA, competitive labor availability, and the growth of electronics, automotive, aerospace, and light manufacturing clusters have made the country a primary consideration for foreign companies looking to establish an operational footprint in North America.

From the outside, the opportunity appears straightforward: form a company, hire employees, begin operations, and participate in this growing industrial ecosystem.

In practice, Mexico does not operate as a single, unified business environment. It operates through multiple independent regulatory authorities, each governing a distinct dimension of how a company exists and functions within the country.

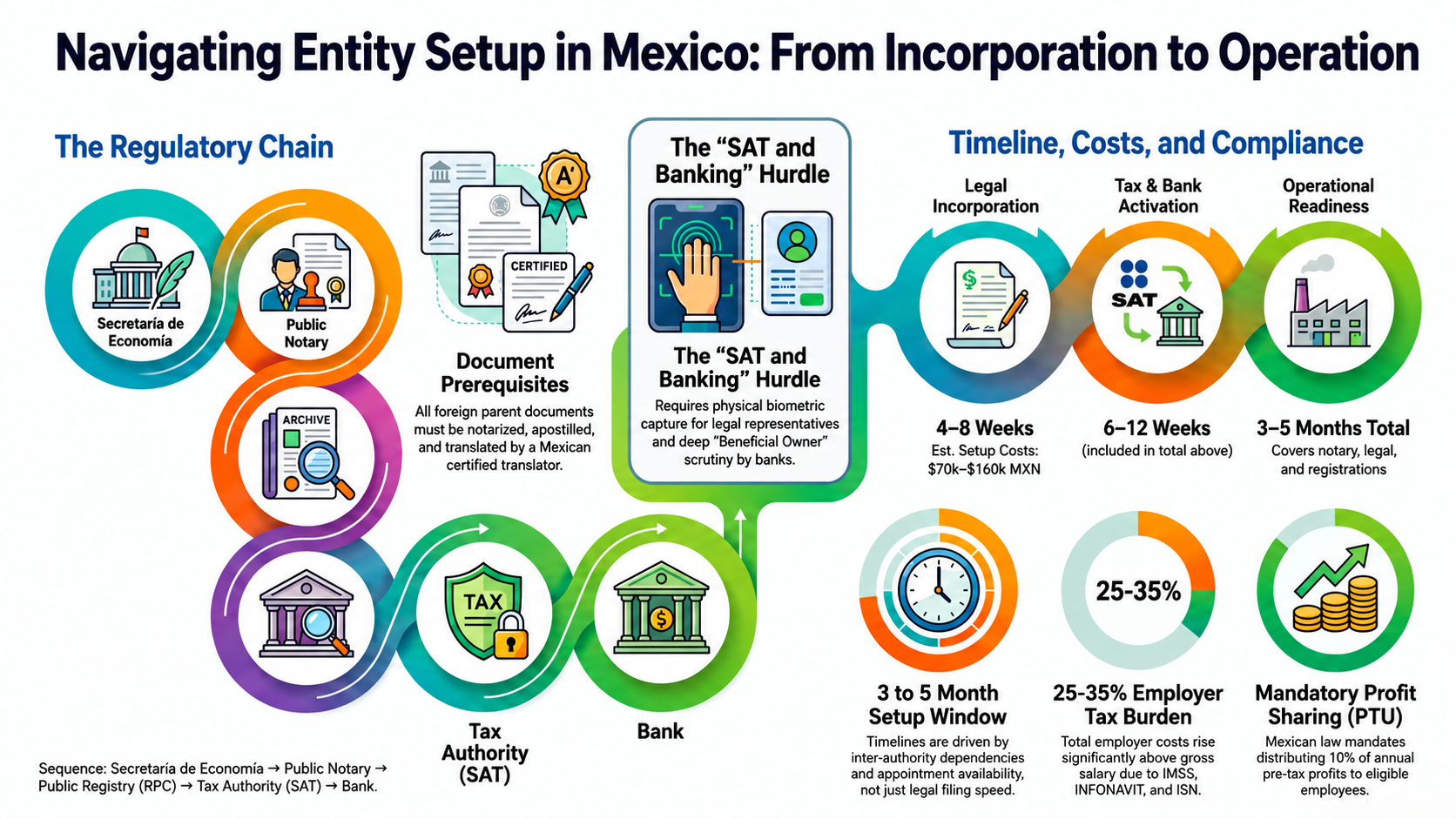

- Corporate existence is governed by the Secretaría de Economía and formalized through the Registro Público de Comercio.

- Tax existence is activated through the Servicio de Administración Tributaria (SAT).

- Employer existence is regulated by the Instituto Mexicano del Seguro Social (IMSS), Instituto del Fondo Nacional de la Vivienda para los Trabajadores (INFONAVIT), and overseen by the Secretaría del Trabajo y Previsión Social (STPS).

- Financial operability depends on corporate bank compliance, including strict beneficial ownership verification.

Incorporation Is Legal Creation. Operational Readiness Is Something Else.

In Mexico, incorporation only creates legal existence. It confirms that the company is recognized as a juridical person and recorded with the Registro Público de Comercio (RPC). At this stage, the company exists on paper as a legal entity. Nothing more.

Legal existence does not grant the company the ability to transact, employ, or operate.

To function in practice, the company must be independently recognized by additional authorities, each responsible for a different dimension of business activity.

Tax existence is established separately through registration and activation with the SAT. Without this, the company cannot issue CFDI invoices, comply with fiscal obligations, or conduct financial transactions in compliance.

Employer existence is governed by registrations with the IMSS and INFONAVIT, and oversight by STPS. Until these are completed, the company is not legally permitted to hire employees, run payroll, or meet statutory labor obligations.

Financial existence depends on passing corporate bank compliance and KYC reviews. Without a Mexican corporate bank account, capital cannot be deposited, payroll cannot be processed, and vendors cannot be paid. Each requires documentation, sequencing, and validation before granting operational legitimacy within its domain. This is why companies often find themselves in a confusing position: fully incorporated, yet unable to hire, invoice, or transact.

The Incorporation Sequence: Why Document Readiness Determines Timelines

In Mexico, incorporation moves forward only when documents are perfectly aligned for the next authority in the chain.

The sequence itself is fixed:

Secretaría de Economía → Public Notary → Registro Público de Comercio (RPC) → SAT → RNIE → Bank

This is where timelines are won or lost.

The process begins with name authorization from the Secretaría de Economía. This approval allows drafting of incorporation documents, but those documents cannot be prepared casually. Every detail inserted here, shareholders, capital structure, corporate purpose, legal representation, will be scrutinized again by the notary, then by the RPC and SAT, and later by the bank.

Before the notary will even schedule incorporation, foreign parent company documents must be:

- Notarized in their country of origin

- Apostilled under the Hague Convention

- Translated into Spanish by a certified translator in Mexico

These are not parallel activities. They are prerequisites. If even one document is missing proper apostille or certified translation, the notary will not proceed.

Only after RPC records the entity does the company gain formal commercial recognition. But even at this point, the entity is still unable to operate.

The next critical dependency is SAT. It requires the legal representative to appear physically for biometric capture. Appointments are limited. If documents from RPC contain even minor inconsistencies with what was drafted earlier, SAT will not activate the tax registration. Corrections here often require returning to the notary and re-registering amendments with RPC before SAT will proceed.

After SAT activation, foreign-owned entities must be recorded with the RNIE within a defined window. This filing depends on the exact incorporation and tax data already registered. Any mismatch creates compliance exposure.

Only then does the bank process begin. Banks do not treat incorporation documents as new information. They compare them against SAT records, RPC data, beneficial ownership declarations, and proof of address. Their KYC review often reopens questions that earlier authorities have already examined. If documentation is not perfectly consistent across every stage, the bank places the application on hold.

Throughout this chain, one factor remains constant: the legal representative must be available to sign, appear, and respond at multiple stages. Delays frequently occur not because of regulation, but because signatures, presence, or clarifications are not immediately available when an authority requests them.

This is why incorporation timelines in Mexico are rarely determined by how quickly applications are filed. They are determined by how prepared the documentation is before the first step even begins.

SAT and Banking: Where Most Foreign Companies Lose Weeks

Appointment availability is limited and often booked weeks in advance. Missing this window can quietly stall the entire setup timeline.

Once issued, the e.firma enables the company to generate CFDI (Comprobantes Fiscales Digitales por Internet)- Mexico’s mandatory digital invoicing framework. Without CFDI capability properly configured, the company may hold an RFC but still be unable to invoice clients or run compliant payroll.

This is where many organizations realize that tax registration and tax activation are not the same thing.

Mexican banks conduct deep Beneficial Owner (Controlador Beneficiario) scrutiny. They do not rely solely on incorporation documents. They cross-check:

- Shareholding structure against SAT records

- Legal representative authority against notarized deeds

- Corporate purpose against expected transaction profile

- Proof of fiscal address against registry data

Banks apply their own compliance lens, independent of what earlier authorities have accepted. If there is any inconsistency in names, addresses, share percentages, or documentation sequence, the file is paused for clarification.

At this point, companies often find themselves in a position where:

- The entity is incorporated

- The tax ID exists

- The digital signature is issued

Yet, financial operations remain blocked.

Mandatory Employer Registrations

Hiring in Mexico is not an HR activity. It is a multi-authority compliance activation.

Before the first employee can be onboarded, the company must be recognized as an employer across several independent systems.

The first is registration with IMSS. It assigns a workplace risk classification based on the company’s declared business activity, which directly influences contribution rates. Payroll reporting, employee healthcare coverage, pension contributions, and social security obligations are all governed through this registration.

Parallel to IMSS is registration with INFONAVIT. Employers are required to contribute to Mexico’s statutory housing fund for employees. This contribution is mandatory, payroll-linked, and frequently overlooked during early planning because it does not exist in many other jurisdictions.

At the labor compliance level, alignment with the STPS becomes critical. Employment contracts, internal policies, workplace documentation, and record-keeping must meet Mexican labor law standards and be inspection-ready. These are not template-driven requirements; they must reflect the company’s registered corporate purpose, risk classification, and payroll structure.

In addition to federal obligations, companies must account for ISN (Impuesto Sobre Nómina)- a state-level payroll tax typically around 3% of total remuneration. This tax is administered at the state level and operates independently of federal payroll contributions.

Then comes one of the most unfamiliar obligations for foreign companies: PTU (Participación de los Trabajadores en las Utilidades). Mexican labor law mandates that 10% of annual pre-tax profits be distributed among eligible employees. This is not discretionary, and it becomes a recurring financial obligation once the company is profitable.

When IMSS, INFONAVIT, retirement contributions, mandatory benefits, and ISN are combined, the true employer cost in Mexico typically rises to 25-35% above gross salary.

There is an additional compliance dimension introduced by Mexico’s outsourcing reform. If the company engages third-party providers for specialized, non-core services, those providers must be registered under REPSE (Registro de Prestadoras de Servicios Especializados). Failure to verify this can create labor and tax exposure for the company itself.

Until these registrations are complete and aligned, the company may be legally incorporated, tax-registered, and bank-enabled, yet still unable to hire compliantly.

Real Timelines and Real Costs

For foreign-owned entities, the realistic end-to-end journey from initiation to being fully ready to hire typically spans 3 to 5 months.

This duration is not driven by legal complexity, but by inter-authority dependency.

A practical flow often unfolds as follows:

- Company name authorization and document drafting may take 1-2 weeks

- Apostille of foreign documents and certified translations can add another 2-3 weeks

- Notarization is dependent on complete, translated documentation

- Registration with the Public Registry cannot occur before notarization

- SAT registration requires completed registry records and a legal representative’s biometric appointment, which is schedule-dependent and can take 2-4 weeks to secure

- Bank account opening runs in parallel but frequently becomes the longest step, often requiring 4-8 weeks due to KYC and beneficial owner verification

- Employer registrations cannot be finalized without SAT credentials and bank readiness

From a cost perspective, organizations should realistically budget $70,000 to $160,000 MXN for the setup phase alone. This range typically includes:

- Notary and incorporation fees

- Legal and advisory support

- Apostille and certified translations

- Government registrations

- Initial tax, accounting, and payroll configuration

These figures cover incorporation and regulatory activation. They do not include ongoing employer contributions, statutory benefits, payroll taxes, or operational expenses once hiring begins.

The reason timelines stretch and costs accumulate is not because Mexico’s system is unclear. It is because the system is distributed across independent authorities, each requiring original documentation, physical presence, and prior registrations as proof before allowing the next step to proceed.

Why Do Companies Face Delays Even After “Following the Process”?

“We incorporated. Why are we still blocked?”

Because incorporation does not activate tax, banking, or employer systems.

“Why can’t we onboard employees yet?”

Employer registrations and payroll compliance must be active before hiring begins.

“Why is the bank asking questions we already answered during incorporation?”

Banks independently re-verify shareholders and beneficial owners, often more rigorously than notaries or registries.

“Why is SAT taking longer than expected?”

Biometric appointments, digital certificates, and tax configuration are time-dependent and cannot be expedited by paperwork alone.

“Why are our documents being reviewed again and again?”

The same shareholder documents are validated separately by multiple authorities. Minor inconsistencies cause repeated rejections.

“Why does our entity structure matter now?”

A structure chosen early affects governance, tax treatment, and banking acceptance later.

What Must Be Ready Before You Even Start

Most delays in Mexico do not begin at the notary, the registry, or the tax office. They begin inside the company, before the process is even initiated.

Do you have apostilled, translated, and internally consistent shareholder documents?

These will be examined repeatedly by different authorities. Any mismatch in names, addresses, or ownership percentages resurfaces at later stages.

Is your corporate purpose precisely defined?

This single paragraph influences tax classification, employer registration categories, and future invoicing capability.

Do you have a compliant registered address secured in Mexico?

This is required across incorporation, tax activation, banking, and employer filings.

Is a local legal representative formally appointed and available for physical appearances?

Several stages cannot proceed without in-person validation.

Is your hiring plan already mapped?

Headcount, payroll timing, and role types affect how and when employer registrations must be completed.

Have you identified your banking partner and capital plan in advance?

Banks do not wait for incorporation. They re-evaluate ownership, documentation, and risk independently.

- Companies that prepare these elements beforehand move through the process methodically.

.webp)

Why This Requires Coordinated Local Expertise

By this point, it becomes clear that setting up in Mexico is not a linear legal task.

It is a sequenced activation across corporate, tax, banking, employer, and labor systems that operate independently and evaluate the same company from different regulatory lenses.

Progress in one area does not accelerate the others.

In fact, misalignment between them is what most often causes delays.

This is why successful market entry is rarely about “getting incorporated” but about ensuring that incorporation, tax activation, banking readiness, and employer compliance are planned, timed, and executed as a single coordinated effort.

This is where E-Solutions operates.

Not as a registration facilitator, but as a coordinator of the entire regulatory sequence required to make a Mexican entity truly operational.

Whether through a GCC model for long-term capability building, a BOOT approach for phased ownership, or a direct entity setup for immediate presence, E-Solutions aligns every authority, document, and milestone into one executable path.

Because in Mexico, the difference between a company that is incorporated and a company that is ready to operate is not paperwork but coordination.

Works Cited

- Secretaría de Economía. Autorización de Uso de Denominación o Razón Social; Registro Nacional de Inversiones Extranjeras (RNIE). Government of Mexico.

- Registro Público de Comercio. Inscripción de Sociedades Mercantiles. Government of Mexico.

- Servicio de Administración Tributaria (SAT). Inscripción al RFC, Obtención de e.firma, y Comprobantes Fiscales Digitales por Internet (CFDI). Government of Mexico.

- Instituto Mexicano del Seguro Social (IMSS). Registro Patronal e Inscripción de Trabajadores. Government of Mexico.

- Instituto del Fondo Nacional de la Vivienda para los Trabajadores (INFONAVIT). Obligaciones Patronales. Government of Mexico.

- Secretaría del Trabajo y Previsión Social (STPS). Normatividad Laboral, REPSE, y Cumplimiento Patronal. Government of Mexico.

- Cámara de Diputados del H. Congreso de la Unión. Ley General de Sociedades Mercantiles. Diario Oficial de la Federación.

- Cámara de Diputados del H. Congreso de la Unión. Ley Federal del Trabajo (Participación de los Trabajadores en las Utilidades - PTU). Diario Oficial de la Federación.

- Secretaría de Hacienda y Crédito Público (SHCP). Impuesto Sobre Nómina (ISN) - Disposiciones Estatales. Government of Mexico.

- Secretaría de Relaciones Exteriores (SRE). Cláusula Calvo en Sociedades con Participación Extranjera. Government of Mexico.

- Banco de México. Disposiciones sobre Identificación del Beneficiario Controlador y Cumplimiento KYC. Government of Mexico.

- Internal Revenue Service (IRS). Entity Classification (“Check-the-Box”) Regulations. U.S. Department of the Treasury.

- Deloitte. Mexico Investment and Nearshoring Outlook Reports. Deloitte Insights, 2024–2025.

- United States Trade Representative (USTR). United States-Mexico-Canada Agreement (USMCA). Office of the USTR.